Introduction

Most people think investing is only for those who already have money. If you have a few hundred dollars sitting around, sure but $5 here and $10 there? That feels too small to matter.

That belief is exactly why millions of people never start. And it’s also exactly why AI-driven micro-investing apps have become one of the most quietly powerful financial tools of this decade. These apps work with the money you already spend every day. They don’t ask you to change your habits, set aside a big amount, or understand the stock market. They just quietly turn your everyday purchases into a growing portfolio and AI makes the whole process smarter than anything a traditional bank could offer you.

This guide breaks down what micro-investing actually is, how artificial intelligence makes it work better, which apps are worth your attention in 2026 and what you can realistically expect to earn over time.

What is Micro-Investing?

Micro-investing is exactly what it sounds like investing very small amounts of money, sometimes as little as a few cents at a time. The concept got popular through round-up investing. The idea is simple: when you buy a coffee for $3.60, the app rounds that purchase up to $4.00 and invests the extra $0.40 automatically. Do that across 20–30 transactions a week, and you’re quietly investing $8 to $15 without ever consciously thinking about it.

Before apps like Acorns made this mainstream, small-amount investing was nearly impossible. Brokerage accounts had minimum deposits of $500 or more, and most investment platforms weren’t designed for people working with small, irregular amounts. Micro-investing broke down that barrier completely.

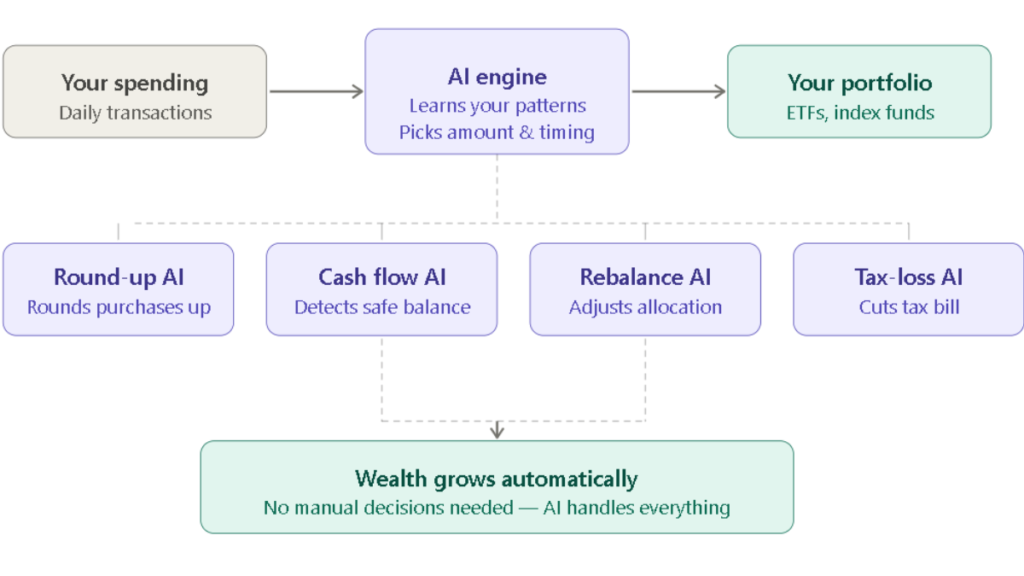

Today, these apps go far beyond simple round-ups. You can set weekly auto-deposits, invest during specific spending triggers, or let AI decide the best time and amount to move money from your checking account into your portfolio.

How AI Makes Micro-Investing Smarter

Standard micro-investing apps from a few years ago were fairly basic they rounded up your purchases and put the change into a pre-set portfolio. That worked, but it had no intelligence behind it. You could overdraft your account because the app didn’t know you had rent coming out. You had no say in timing. And every user got the same generic portfolio regardless of age, income, or goals.

AI changed all four of those problems at once.

Modern AI-powered micro-investing apps analyze your income and spending patterns continuously. They learn when your paycheck hits, when your major bills go out and what your safe balance is. Instead of blindly pulling money every day, the AI waits for a financially healthy moment before investing so you never get caught short.

The intelligence also works at the portfolio level. Based on your age, risk tolerance, and how long you plan to invest, the AI allocates your contributions across different asset types usually a mix of stock ETFs and bond ETFs. When the market shifts or your portfolio drifts from its target, the AI rebalances automatically. Some apps even apply tax-loss harvesting, a strategy where losing positions are sold at a loss to offset gains and reduce your tax bill a feature that used to be exclusive to expensive wealth management services.

The result is a system that genuinely manages itself. You don’t need to know what an ETF is you don’t need to watch market. You just connect your account and let the AI do the rest.

Top AI Micro-Investing Apps in 2026

There are several solid options available right now, and each one suits a slightly different type of user.

Acorns:

Remains the most popular entry point for beginners. It pioneered the round-up model and has since added AI-driven “smart deposit” features that analyze your cash flow before pulling any money. The interface is clean and simple, and the investment portfolios are built by Nobel Prize-winning economists. Acorns charges $3/month for its personal plan, which also includes a checking account and retirement account access. For someone investing $20–$30 a month, that fee is something to consider but for users who also use the retirement and checking features, the value is solid.

Stash:

Takes a different approach. Rather than only using round-ups, Stash lets you choose individual stocks and ETFs alongside automatic investing. Its AI feature called “Smart Portfolio” monitors your selections and nudges you toward a more balanced allocation when you’re overexposed to any single sector. Stash charges $3/month for its basic plan and $9/month for access to custodial accounts for kids. It’s well suited to people who want some control over what they invest in, without having to do all the research themselves.

Plum:

Has become particularly popular in the UK and is expanding globally. Its AI algorithm, known as the “Plum Brain,” monitors your transaction history and automatically sets aside small amounts of money every week calculating the exact amount you can afford without impacting your regular life. What makes Plum distinctive is that it feels less like an investing app and more like a financial assistant. It helps you save, invest, and budget all in one place. The basic version is free, with premium features available for a monthly subscription.

Robinhood’s Recurring Investments:

Feature, while not a dedicated micro-investing app, deserves a mention because of its zero-commission structure. You can set up automatic weekly purchases of fractional shares in individual stocks or ETFs for as little as $1. The AI component here is lighter than Acorns or Plum, but for users who want to build a stock portfolio gradually without paying fees, it’s worth considering.

Betterment:

operates at a slightly higher level than the others but it still accepts small initial amounts and uses some of the most sophisticated AI-driven portfolio management available to retail investors. Its tax optimization and automatic rebalancing features are among the best in the industry. Betterment charges 0.25% annually rather than a flat monthly fee which actually makes it cheaper than flat-fee apps once your balance grows past a certain point.

How Much Can You Actually Earn?

This is the question everyone wants answered honestly, so here it is with realistic numbers, not marketing claims. If you invest $10 per week consistently through a micro-investing app, you’re putting in roughly $520 a year. Assuming an average annual return of 7% (which is close to the historical average for a diversified stock portfolio), here’s how that grows:

After 5 years, your total contributions would be around $2,600. With compound returns, your actual balance would be closer to $3,100. After 10 years, contributions of $5,200 grow to approximately $7,200. After 20 years, $10,400 in contributions grows to around $26,000. The numbers look even better if you increase your contributions over time as your income grows. Someone investing $20 a week for 20 years at the same return rate ends up with approximately $52,000 from money they largely never noticed leaving their account.

The key factor here is time, not the amount. Starting at 22 instead of 32 with the same contributions nearly doubles your final balance thanks to compound interest. This is why micro-investing apps emphasize getting started over getting started big. One honest caveat: these projections assume consistent market returns and don’t account for app fees, which can meaningfully reduce returns when your balance is small. A $3/month fee on a $300 balance is 1% annually significantly higher than what you’d pay at Betterment or Vanguard. As your balance grows, percentage-based fees usually become more cost-effective than flat monthly fees.

Risks to Know Before You Start

Micro-investing is genuinely low-risk compared to active stock trading, but it’s not without its considerations. The biggest misunderstanding is treating it as a replacement for an emergency fund. Your investments are exposed to market fluctuations, and if you need to withdraw during a downturn, you could get back less than you put in. Always keep 3–6 months of expenses in a regular savings account before investing, even though an AI micro-investing app.

Fee drag is another real concern for small balances, as mentioned above. If you’re only investing $15 a month and paying $3 a month in fees, 20% of your money is going to the platform. This isn’t a reason not to start but it is a reason to increase your investment amount as soon as you’re able, or switch to a percentage-based fee platform once your balance exceeds a few thousand dollars.

There’s also the question of investment type. Most micro-investing apps put your money into diversified ETF portfolios, which is generally smart. But if you’re drawn to apps that let you pick individual stocks or crypto, the risk profile changes significantly. AI can help with analysis, but no algorithm predicts individual stock movements reliably.

Finally, these apps are not a substitute for a retirement account. Once you have a stable income, contributing to a 401k (especially if your employer matches contributions) or an IRA gives you tax advantages that a standard micro-investing account simply cannot match.

Setting Up Round-Up Investing

Getting started takes less than 10 minutes with most apps. Here’s a straightforward process that works across most platforms. Download your chosen app and create an account with a valid email and phone number. You’ll need to verify your identity with a government-issued ID this is standard for any regulated financial service and takes a few minutes with AI-powered ID verification built into most apps.

Connect your primary checking account or debit card. This is the account the app will monitor for round-ups and from which it will pull your investment contributions. Most apps use read-only connection services like Plaid, which means the app can see your transactions but cannot move money without your permission. Choose your investment portfolio. If you’re unsure which to pick, most apps will walk you through a short questionnaire about your age, goals, and comfort with risk, then recommend one automatically. For beginners, a moderate or conservative portfolio that mixes stocks and bonds is a sensible starting point.

Set your round-up multiplier. Most apps let you choose between 1x (standard round-up), 2x, or 3x. A 2x multiplier means your $3.60 coffee round-up becomes $0.80 instead of $0.40. This is a simple way to invest more without changing any behavior. Finally, consider adding a small weekly recurring deposit even $5 or $10. Round-ups alone are unpredictable in amount. A small recurring deposit alongside your round-ups gives your portfolio more consistency and accelerates growth noticeably over time.

FAQ‘s

Q1. Is micro-investing safe for beginners with no investment knowledge?

Yes. The apps handle all investment decisions automatically. You don’t need to understand the stock market to use them. Your money goes into diversified portfolios managed by algorithms, which reduces the risk that comes with picking individual investments.

Q2. How much money do I need to start?

Most AI micro-investing apps have no minimum balance requirement. Acorns, Stash, and Plum all let you start with $0 and begin building from your first round-up. Some apps like Betterment ask for a $10 initial deposit to activate automated investing.

Q3. Will micro-investing affect my day-to-day spending?

Not if the app is working correctly. The AI in modern apps specifically monitors your cash flow to avoid investing when your account balance is low. If you ever feel the withdrawals are affecting your budget, you can pause or reduce them within the app at any time.

Q4. Do I pay taxes on the money I earn through micro-investing?

Yes. Any gains or dividends earned in a standard investment account are subject to capital gains tax. However, if you use a micro-investing app that offers an IRA account (like Acorns Later or Betterment’s IRA), those earnings can grow tax-deferred or tax-free depending on the account type.

Q.5 Can I withdraw my money whenever I need it?

Yes. Your money is not locked in. You can request a withdrawal at any time, and most platforms process it within 3–5 business days. Keep in mind that withdrawing during a market downturn means selling at a lower price than you bought so the longer you can leave the money invested, the better.

Conclusion

The idea that investing is only for people with large sums of money is outdated. AI-driven micro-investing apps have completely removed the barrier to entry, making it possible for anyone to build wealth through the small amounts they already spend every day.

The AI behind these platforms doesn’t just automate round-ups it learns your financial habits, chooses the right moment to invest, manages your portfolio intelligently, and even handles tax optimization. What used to cost thousands of dollars in financial advisory fees is now available for a few dollars a month, or in some cases, for free.

The most important step is simply starting. Even $5 a week, invested consistently over 15–20 years, can grow into a meaningful sum thanks to compound returns. Pick an app that matches your comfort level, connect your account, and let the AI handle the rest.

Wasim Akram is the Founder of LuxuryGole and a dedicated Tech Expert with over 10 years of experience in the digital ecosystem. Specializing in smartphone optimization, hidden software hacks, and digital security, Wasim focuses on providing premium, actionable insights to help users master their technology. His decade-long journey in the tech space ensures that every guide on LuxuryGole is backed by deep research and practical expertise. Connect with him on LinkedIn and Facebook for daily tech updates